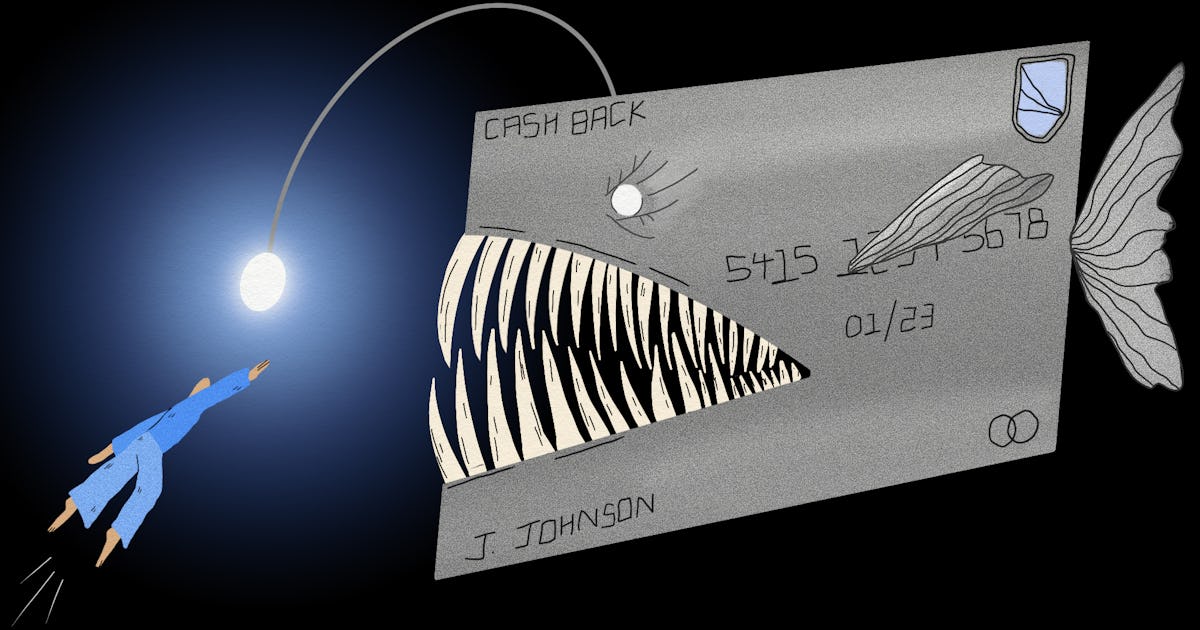

BBB says stay independent of payday lender debt cycle Consumers can easily fall into the debt trap, especially as inflation appears to be eroding purchasing power. Payday loans can be attractive when you’re on the downside of the debt cycle, but your Better Business Bureau (BBB) advises extreme caution. Take a few moments to think about how your debt could skyrocket even as you try to defuse a precarious financial problem. For those with credit problems, payday lenders have enormous appeal. Bank lenders and credit card companies may not be an option, forcing you to turn to the quick fix of a payday loan. These loans, however, come at a huge cost. Their exorbitant interest rates can force you into a continuous cycle of renewing this loan, paying new fees every two weeks, digging a deeper and deeper hole. Video ads for these lenders are now appearing on TikTok, trying to appeal to a new, younger audience. Loans are made to look cheap and easy. The claims made are often dishonest and can trap those unaware of the deception. Personal Loans Explained Here’s what personal loan ads don’t tell you: • Loans are expensive. The Consumer Protection Bureau says interest rates from these lenders are in the stratosphere, at almost 400%. Even high credit card interest rates are only around 30%. • Just because the loan is easy to get doesn’t mean it’s a good idea. Research other options. They target you if you’re young or have bad credit, touting “no credit checks” or other documents. • Social media ads are unreliable. Too good to be true ? He is. Never take claims made in social media ads at face value. Do your research. • Make sure you can repay the loan. Their high interest rates can trap you. Your inability to repay the loan can further ruin your credit. • You should never pay upfront fees for a loan. Never pay with a post-dated check to cover the amount borrowed plus interest. • Walk away if they ask for fees paid upfront and in cash. The same applies to requests by bank transfer. • You should only borrow what you know you can repay with your first paycheque. When they allow you to “carry over” the balance from one week to the next, they add an additional charge. Next thing you know, you owe a lot more than you originally needed. • You have rights. They are required by law to disclose your rights before granting you the loan. This should include the cost, interest rate and all other charges. Anything can be in the fine print, and you should read it all. • You must keep all documents. Some report receiving calls from collection agencies years after the loan was paid off. Keep your proof that you repaid the loan. • You should check all companies you are considering using on bbb.org. • If you are treated unfairly, you must report it to the Federal Trade Commission and the BBB. Better alternatives If it’s not too late, prepare a spending budget with an emergency fund. Setting aside even a small amount of money with each paycheck can help you overcome a difficult financial situation. If you need a loan, shop around. Look at interest rates, fees and late charges, all found in the fine print that only smart customers read. Credit unions are always a good place to check for small loans that have reasonable fees. Even credit card advances can be better than payday loans. Remember to contact creditors if you cannot pay on time. Many will work with you to work out a payment plan. For answers to other questions about payday loans and their alternatives, contact BBB at (800) 856-2417 or visit our website at BBB.org.

BBB talks payday lenders

/do0bihdskp9dy.cloudfront.net/07-07-2022/t_6229e64e839b45f989d4f75b87104399_name_file_1280x720_2000_v3_1_.jpg)

/do0bihdskp9dy.cloudfront.net/07-07-2022/t_6229e64e839b45f989d4f75b87104399_name_file_1280x720_2000_v3_1_.jpg&description=BBB%20talks%20payday%20lenders){kind=link}